For any business, inventory is a vital component on which the company depends. So, inventory management is making sure you keep track of the inventory. It keeps your inventory organized so you don’t have to spend a long time searching for a particular product in your business when you need it.

Even though it is an important part of your business, not everyone can effectively conduct inventory management. Only 63% of businesses can accurately track their inventory, which means over 30% of businesses don’t know what is happening to their inventory before it is too late!

So how do you solve that? The answer is inventory management strategies. In this article, I will share what are the important inventory management strategies that you can apply to your business so you can avoid being in the 37% business who don’t know how to manage their inventory.

What Is Inventory Management? – The Process And Importance

We got introduced to the concept of inventory management so now let’s get into what is involved in the inventory management process:

Inventory Management Process

Inventory management is made up of 4 different components in the process for managing your inventory:

- Inventory Tracking: At the heart, inventory management is keeping track of goods.

- Procurement and Replenishment: Next up is the procurement and replenishment. What this means is where you get your inventory from and how you will get new inventory to replace what you have sold

- Quality Control and Shelf Life Management: Once you have the inventory in your business or warehouse, inventory management is all about taking care of the products. This requires ensuring the maintenance of their quality and the way they are presented to the customers.

- Sales and Distribution Planning: It is not just about keeping appearance with the inventory, the management side of inventory also takes into account how you sell and ship the products to your customers.

Why Is Inventory Management Important?

The importance of inventory management is simple: the better you manage your inventory, the easier it is for you to do business. For example, you have an inventory of 500 toys. You are expected to sell about 450 of them, but later you discover that 100 of the toys are missing, damaged, or not the right toy you ordered. So now, you are 50 toys short of meeting customer demand and have also paid for 100 toys than you should have.

In instances like this, inventory management helps you negate these types of issues. At its core, that is what makes it so important for a business to take care of its inventory. There are more reasons why inventory management is important for your business.

13 Important Inventory Management Strategies For Better Inventory Control

Inventory management strategies are there to tackle all your inventory needs, but which ones are important for all businesses? Here are some of the important strategies that you need to know about:

Strategy#1 ABC Analysis

Probably the most important inventory management strategy is doing ABC analysis. ABC analysis is where your business categorizes inventory under different specifications. For example, A-items typically represent a small percentage of total inventory but contribute a significant portion of revenue. These high-value items require closer attention to ensure availability and minimize stockouts. B-items are moderately important, while C-items are low-value and may have lower stocking priorities.

So how does this help? It lets you know which inventory products you need to prioritize over others. If product A is running low, then you know that you need to restock it immediately. On the other hand, product C does not require to be immediately replenished when it reaches below safety stock levels. With this information, you can strategically account for your inventory in a way to optimize your inventory and sales.

Strategy#2 Just-In-Time Stock

Just-in-time stock is when you replenish stock on a needs basis. For example, if your inventory is running low, you know you need to buy more. Then, you can strategize beforehand to ensure that you have inventory just in time before it needs to be put on store shelves or shipped.

Just-in-time stock helps maximize your inventory efficiency. Instead of overstocking your product, you are ordering inventory just in time when they are needed. This allows you to minimize excess inventory and reduce storage costs. You have inventory just in time to fulfill customer demand so your inventory does not become dead stocks.

However, it is a tricky inventory management strategy to implement. It requires a coordinated effort from all over the supply chain to synchronize inventory with customer demand. It might be risky, but the strategy allows your business to increase sales and reduce overhead costs at the same time.

Strategy#3 Safety Stock Management

Safety stock level is when you have a set amount of inventory you need to have before you need to reorder them again. Safety stock management is all about handling and making sure your inventory is always at optimal levels, so you don’t run the risk of being understocked or overstocked.

There is a lot that goes into safety stock management. You need to coordinate demand variability, supplier reliability, and production lead times to ensure you have enough products on hand for sales or shipping. Holding inventory incurs a cost that you need to bear, but it is much easier to have stock in hand and helps mitigate the risk of stockouts and other inventory management challenges.

Strategy#4 FIFO And LIFO

FIFO (First-In, First-Out) and LIFO (Last-In, First-Out) are how you want to sell your inventory. In FIFO, it is all about selling the inventory that comes first. It is great for food and other perishable foods that have a time-sensitive period that needs to be sold before they spoil. LIFO is the complete opposite, as you are selling the newest inventory first and holding old inventory for sale later.

Both have their advantages. FIFO is great for a fast-paced industry where products are on a timer before they cannot be sold. The food industry uses FIFO to ensure customers are getting the freshest products possible. LIFO holds the products in hand and can be sold in the future. This is especially good for industries where prices will gradually rise over time. While you are holding these older inventories, you are also reducing your taxable income because these goods do not account for your revenue.

Strategy#5 Demand Forecasting

If you don’t know the future demand for your products, then implementing inventory strategies will be pointless. That is why demand forecasting gives you an advantage in handling your inventory. Think of demand forecasting as a weather reporter. They analyze historical data and market trends to predict what the future demand for products might be.

Knowing the demand beforehand gives you a strategic advantage when you are ordering inventory. It optimizes your inventory levels, minimizes stockouts, and also ensures you are not over-ordering your inventory. Add advanced forecasting using statistical models and AI machine learning and you can forecast product demands in real-time.

Strategy#6 Minimum Order Quantity (MOQ)

Minimum order quantity, or MOQ, is an inventory management strategy that deals with product procurement. It represents the lowest quantity of a product that a supplier is willing to sell in a single order. MOQs from suppliers give you the advantage of discounted prices on bulk purchases to maintain sufficient inventory. MOQ in wholesale provides much more flexibility in inventory purchase so you can lower the cost of product procurement to invest in other aspects of inventory management strategies, like in an inventory management system.

Strategy#7 Economic Order Quantity (EOQ)

Economic order quantity, or EOQ, is all about maintaining optimal order quantity to minimize total inventory costs. Whenever you order new inventory, EOQ calculates how much inventory you need against what the consumer demand would be.

So what does EOQ do? EOQ balances two primary types of inventory costs: ordering costs and holding (carrying) costs. It brings a balance between ordering costs and holding costs. For example, ordering smaller quantities more frequently reduces holding costs but increases ordering costs because of frequent transactions. However, ordering larger quantities less frequently reduces ordering costs but increases holding costs due to higher inventory levels.

So, EOQ calculations identify the order quantity that minimizes the combined impact of these costs, helping businesses maintain efficient inventory levels without overstocking or stockouts. So what you end up with is an efficient order fulfillment having the right amount of inventory to meet customer demand.

Strategy#8 Reorder Points

Reorder point represents the inventory level when you need to replenish it. It takes into account the lead time, customer demand, and safety stock levels to get an accurate measurement of when you need to reorder inventory.

To ensure that new inventory arrives before reaching below the safety stock level, you typically set this reorder point above the safety stock level. By setting appropriate reorder points, your business can ensure timely replenishment, minimize stockouts, and maintain optimal inventory levels to meet customer demand.

Strategy#9 Real-Time Inventory Tracking

Knowing what you currently have can greatly improve your inventory management. Here, real-time inventory tracking takes away the guesswork you might have to do with your current inventory levels. For example, your business can use barcode scanners, RFID tags, and inventory management software to monitor inventory levels and movements continuously.

This gives you real-time visibility of your inventory, allowing you to track when inventory is taken away and when it is restocked. Your business can also offer order tracking services for your customers when you know where the inventory currently is.

Strategy#10 Inventory Audits

Just like with real-time tracking, regular inventory audits are an inventory management strategy to verify your inventory levels. Regular audits help identify discrepancies, detect errors, and prevent inventory shrinkage due to theft or damage.

You can conduct inventory audits through cutoff analysis or physical inventory counts so that they match with what is on paper. Audits are the only way to remove uncertainties regarding your inventory. You can do it in-house or have a third-party audit agency conduct it for you.

Strategy#11 Consignment Inventory

Maintaining large inventory, especially in multiple locations, is a logistical nightmare. Buying and selling in bulk does that to your business. So if you want to reduce the burden on your business, you could sign up for a consignment inventory with a vendor instead.

For example, if you are a wholesale business, you give the goods to a retailer for them to sell. Until the product is sold, you maintain ownership of it. The retailer only pays for the goods upon sale, reducing the financial risk and inventory carrying costs.

Consignment arrangements benefit both parties by improving cash flow, reducing stockouts, and minimizing excess inventory. It’s difficult to maintain without having complete trust in your customers, so do note that it is difficult to maintain consignment inventory for long periods.

Strategy#12 Dropshipping

Now let’s think of the reverse. You are the retailer in question but you don’t have the capacity necessary to hold inventory. So instead, your supplier takes care of everything for you. They hold the inventory and have it shipped to customers for you. That is dropshipping, the e-commerce fulfillment solution for your inventory.

All you do is act as a store where you receive orders from customers. After your customer places an order, you transfer it to the dropshipping supplier who takes care of the rest. You let the supplier handle all inventory management while you gain profits based on the resale value you set on your store.

Strategy#13 Automation And Technology Integration

The industry is changing all the time. The introduction of artificial intelligence (AI) to the public changed everything. In inventory management, automation is helping make it much easier to manage large inventory levels.

Using technology can streamline inventory management by automating tasks such as order processing, inventory tracking, and demand forecasting, and reducing human error in inventory management.

With that, advanced technologies like RFID, IoT sensors, and artificial intelligence enable real-time monitoring, predictive analytics, and proactive decision-making to optimize inventory levels. With the right technology, you can level up your inventory management and utilize a wide range of strategies.

Benefits Of Good Inventory Management Strategies

So what do good inventory management strategies give for your business? Here are the benefits you get:

- Reduced carrying costs: Efficient inventory management minimizes carrying or holding costs, while also reducing unnecessary costs.

- Improved cash flow: With reduced cost, you have more free capital to allocate for investment in growth opportunities or operational improvements.

- Minimized stockouts: Accurate demand forecasting and inventory replenishment strategies reduce the risk of stockouts.

- Lowered excess inventory: Prevents overstocking, minimizing excess inventory that can lead to write-offs, markdowns, or storage costs.

- Enhanced customer satisfaction: With better inventory management, order fulfillment is much faster, improving customer satisfaction.

- Increased efficiency: Streamlined inventory processes and automated workflows improve operational efficiency and reduce manual errors

- Better decision-making: Access to real-time inventory data and analytics enables informed decision-making regarding purchasing and inventory procurement.

- Stronger vendor relationships: Effective inventory management helps build stronger relationships with vendors and suppliers, making tricky inventory management strategies easier and more effective.

- Compliance and risk mitigation: Audits and real-time tracking reduce risks like theft and damage while also minimizing human error.

- Competitive advantage: Managing your inventory better gives you a greater competitive advantage over your competitors.

Implementing Inventory Management Strategy With A Bulk Order App On Shopify

Strategies are great for the planning section, but how do you put them into practice? For traditional retail businesses, it is easy because you can physically manage your inventory. But in e-commerce, the same can’t be said.

Keeping track of inventory online can seem difficult but inventory management software will help solve the issue. But remember, inventory management is also about handling sales. The inventory management software helps you keep track of everything but does not necessarily help sell it.

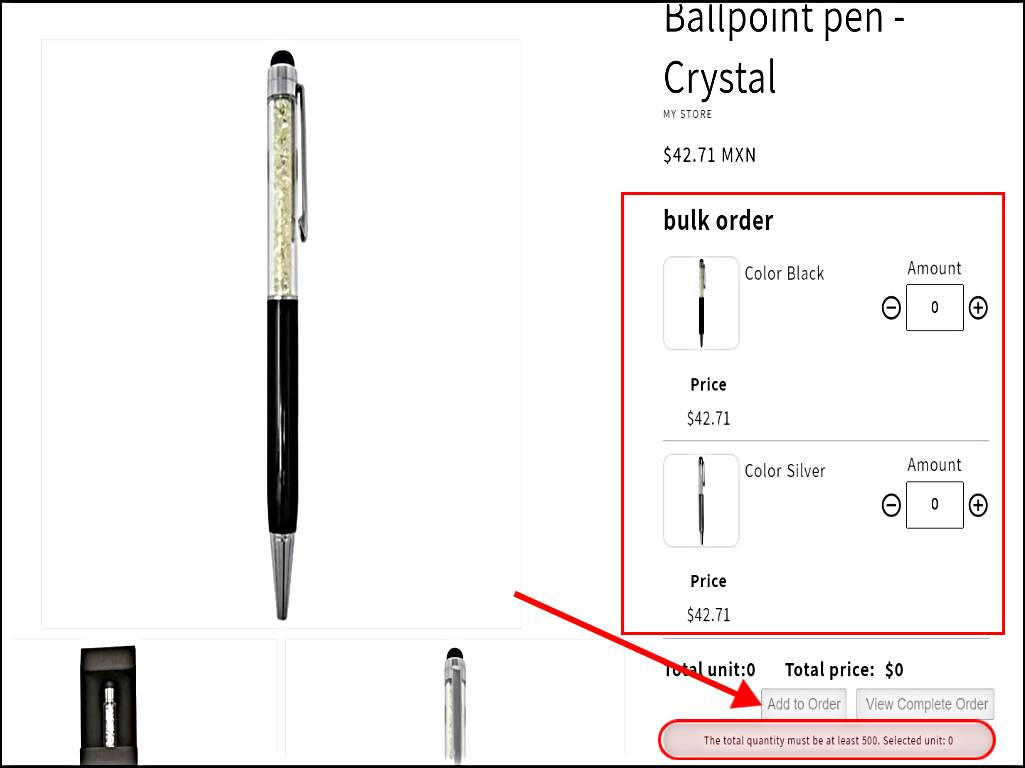

But I can give you an example of one app that can help you both manage inventory and produce sales for your e-commerce business on Shopify! Here is the Shopify store using a bulk order app to help increase sales:

You can see the app shows available variants in a customized display option. The store owner gets to choose how the product variants are displayed. Here, the customers of the store can choose how many variants they want to order. However, there is a catch. At the bottom, you will notice there is a message stating: Total quantity must be at least 500. This is the MOQ or minimum order quantity set on the product. If the customers don’t meet this minimum requirement, the add to order button will be grayed out and they won’t be able to select it.

So how does this app help with inventory management strategies and improving sales?

- It shows all the product variants on one page so customers don’t have to switch between product pages

- MOQ is a key part of inventory management strategies, but implementing one on Shopify is not possible with just the native options. But with the app, you have a MOQ restriction for your products, which is not possible with native Shopify options.

- All quantity selections are made on one page and added to the cart in one click for ease of shopping, making customers more likely to buy your products

- Buttons are grayed out until the MOQ restriction is met. Customers don’t accidentally add the wrong amount to their orders, simplifying the shopping process further.

With one app, you can implement an important inventory management strategy while also making sure customers are enjoying the simplicity of shopping in your store. Your customers are happy and you get to manage inventory and improve sales simultaneously.

Bottom Line

Inventory management strategies are there to help you manage your inventory in a way to maximizes your business’s efficiency. Many strategies might or might not be suitable for your business. That is why I have included the important strategies that you can combine to form a successful inventory strategy tailored to your business. Hopefully, you now know more about what strategies will help bring success to your business’s future.